Stay informed about freight market conditions and other factors that can impact your supply chain. In this Market Update, we cover the following: Truckload, Less-Than-Truckload, Intermodal and International (Ocean & Air).

MARKET UPDATE OVERVIEW

The Coronavirus (COVID-19) threw a level of uncertainty into 2020 for the transportation industry with ongoing constraints into 2021.

Although our economy is poised for growth this year, the acceleration we have experienced over the last six months has impacted the timeline of capacity and the ability to meet demand is a continuous challenge across the transportation market.

We continue to see a decline in the service sector with growth in the durable goods sector. As the service sector begins to normalize, we anticipate a rebound for this sector within Q3 and Q4.

The overall common theme for 2021 as it relates to the transportation industry is capacity will remain tight and it will have an impact on cost constraints and cost increases. In the remainder of this blog, we will take a deeper dive into the core services by SUNTECKtts to gain a better understanding of market impacts.

TRUCKLOAD UPDATE

Truckload volumes were strong at the start of the year with tight capacity. In mid-February, we had a significant weather event causing volumes to shoot up quickly and the demand has only increased throughout Q2.

As a reminder, carriers reject loads on contracted pricing for two reasons. They either truly do not have capacity, or the rates have climbed to a point where they are servicing other shippers at high spot market rates vs contracted rates. It would appear that things were starting to calm down until the weather event in February. Although tender rejections were trending down, carriers were still at an extremely high rejection rate of 20%.

What we have discussed thus far is what has already occurred, let us now review a few items to be aware of. It is clear weather has had a huge impact; however, the Truckload market was already struggling with capacity due to driver shortages and changes to insurance requirements.

One of the primary reasons we keep hearing about driver shortages not improving is The Drug and Alcohol clearinghouse rules. They are now preventing drivers from going to a new carrier to get hired immediately after being fired for drug and alcohol issues from their previous employer. Last year there were over 56,000 violations and of those violations 45,000 lost their jobs. The drivers are given an opportunity to complete a return-to-work program to begin driving again. The most concerning stat that we are seeing is 75% of drivers who lost their jobs have not completed the program. While we agree with the clearinghouse rules, it has resulted in a high number of drivers being removed from the market within the last year.

Another item to be aware of is insurance changes. The cost of insurance for owner-operator and trucking companies is high and still rising. The minimum insurance requirements are being reviewed and could potentially increase from $750k to $2 Million. If that passes, it could cause a number of trucking companies to shut down and rates to go up immediately.

LESS-THAN-TRUCKLOAD UPDATE

As you can imagine, the truckload market tends to impact what we see in the LTL market. When truckload costs spike, shippers will start to push the envelope on larger LTL shipments to avoid having to pay higher rates. Sometimes it is simply a capacity issue where they are unable to locate a truck in a given lane, so they look to LTL. Additionally, LTL is directly impacted by purchased transportation. Carriers will look to the linehaul network for purchased transportation to keep from getting their equipment out of balance, or simply when volumes spike, they have additional options.

When we see service issues with LTL carriers it is important to keep in mind just how vastly different the amount of capacity is from Truckload to LTL. Due to the barriers to entry, there are no new LTL carriers of size entering the market. Occasionally you may see a startup with a consolidation model, however, most are brokering LTL freight to carriers with capacity.

LTL rates are currently on the rise. The LTL blanket pricing programs are used by carriers as a dial to turn volume up in a given market when they want it and turn it down when they don’t. One way they do this is by adjusting the pricing. This year we are expecting national carriers to take sizable price increases. This can vary by lane and depend on the carrier. Some carriers are standardizing the base rates across all blanket programs. When this occurs, lane rates often double.

The other method to reduce volume would be to put embargos in place. The hot spots are Southern California, Oregon, Oklahoma, Texas, Tennessee, Chicago, Pennsylvania, and New Jersey – and as discussed when one carrier makes a change it impacts others quickly. One part of purchased transportation that many large LTL carriers have historically relied on is Intermodal for their linehaul capacity.

INTERMODAL UPDATE

As with other modes, intermodal demand has been very strong since early summer of 2020 and will continue well into 2022. Intermodal services are experiencing challenges with a surge in domestic and international volume. The large increase in volume has created an environment where majority of North American railroads are at capacity. Within all rail networks, to allow trains to effectively move each week, it is critical to keep operations fluid. To do so, many railroads have implemented changes to their intermodal operations. One change we have seen is precision railroading. Precision railroading allows longer trains to continue running from one origin to the next with limited stops. This is an effort to streamline processes to ensure consistent transit. While the current service can be seen as less then desirable, these efforts will lead to much more consistent intermodal service in the future.

The job of intermodal marketing companies (IMC) has become much more complex over the past two years. Railroads are now requiring the IMC to execute the following:

- Reserving equipment

- Reservations to bring a shipment into an origin rail ramp

- Have a shipment depart a destination ramp within 24 hours of arrival (regardless of if the railroad was on time)

- Manage a seamless product to customers

Because of these changes, it is taking a significant amount of time to execute a proficient intermodal shipment.

Throughout 2021, we have seen upward pressure on rates from all intermodal providers, in linehaul increases and accessorial increases. Additionally, we are seeing some carriers exit lanes altogether simply because the lanes do not match their network. As we move forward into Q2, we expect pricing will continue to increase. Price changes will have more of an effect on new users than long-term users of intermodal services. You can also expect accessorial costs to increase to assist the railroads in improving the utilization of containers and keeping the terminals operating fluidly. Some railroads have already instituted their Peak Season Surcharge and those charges will most likely remain in place throughout 2021.

Shippers should expect that there will conversations about potentially changing transit times to ensure more consistent on time performance and that the North American rail network will continue to see increased volume. The high volume leads to challenges, but with planning and dialog, service issues can be minimized.

INTERNATIONAL: OCEAN & AIR UPDATE

When it comes to the current international market condition, there are two primary drivers – extremely high demand from US importers and the ocean carrier’s collective reaction to elevate rates to record high levels.

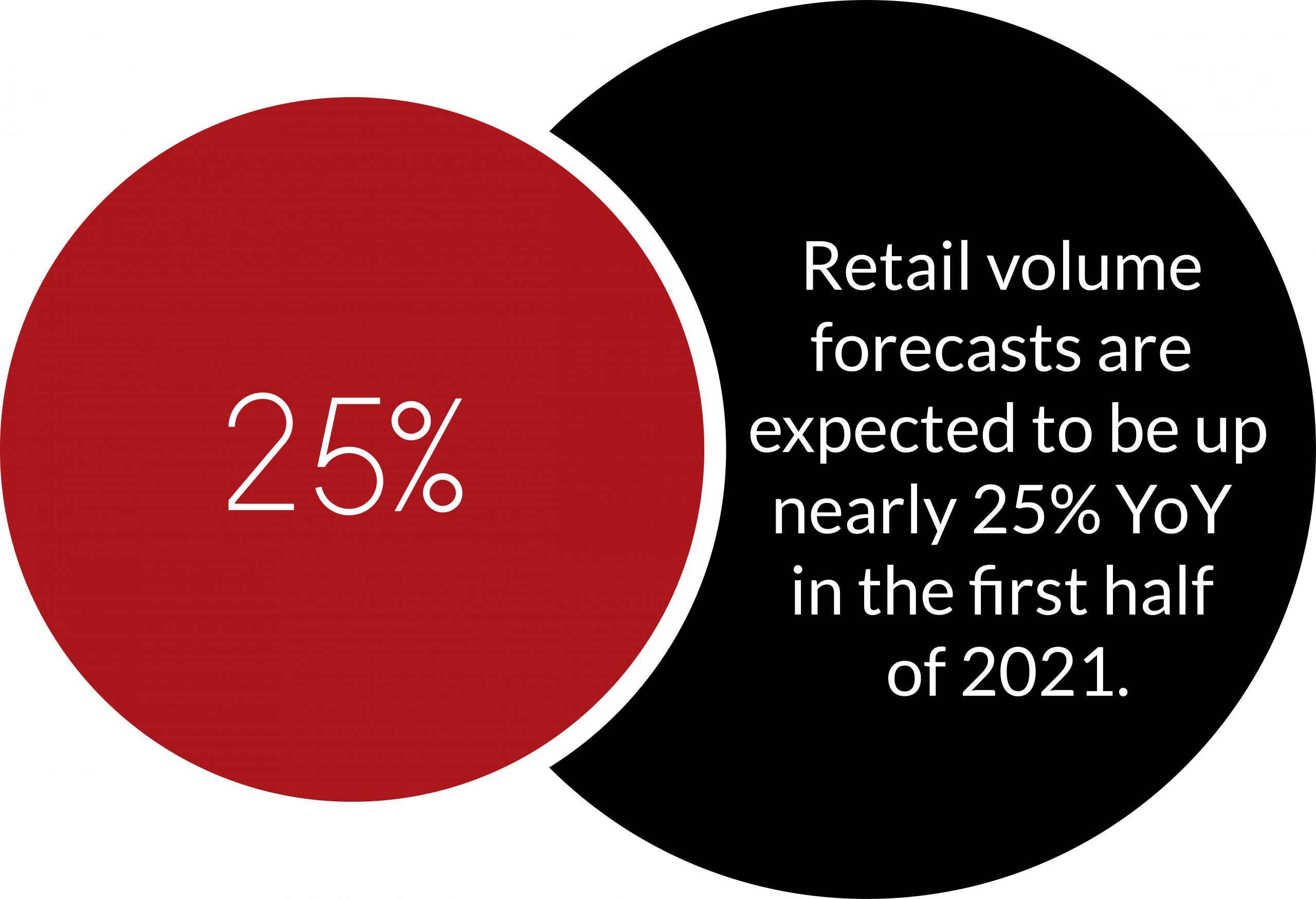

Fueled by consumers being at home more during quarantines and government stimulus money, the retail segment has seen incredible sustained volume demands starting in Q3 2020. Retail volume forecasts are expected to be up nearly 25% YoY in the first half of 2021. Some are predicting similar levels extending well into the second half of the year. The vast majority of these high demand retail items (home furnishings, furniture outdoor items, fitness equipment, electronics, etc.) are sourced by US importers from Asia. This huge spike in demand has put a serious strain on the Trans-Pacific container trade.

The ocean container trade has struggled to handle this volume increase and has reacted by pushing ocean rate levels to record highs, which have remained high for several months. Although Trans-Pacific Ocean spot rates have stopped climbing, and in some cases pulled back slightly, the rates remain at record high levels.

As a result, three categories of ocean carrier rates have emerged in the market and are being offered by carriers to handle volumes. Contract rates, FAK (Freight All Kinds) spot rates and now “premium” rates. These “premium” rates which are thousands higher than FAK spot levels are essentially rates based entirely on shipper’s urgent need to move more volume and a willingness to pay whatever it takes.

Importers have shown no slowdown in their demand for more volume even in the face of these unprecedented rate levels. Available capacity is extremely tight on all Asia to US services. Booking delays and cargo rolls are significant. Empty equipment shortages in Asia are also a serious concern as many US importers are holding containers longer and carriers struggle to get empties loaded on vessels to get back to Asia.

One ongoing threat is port congestion and slower throughput at most major US ports to handle volumes coming in faster and with larger vessels. Ports of Southern California has suffered the worst congestion it has ever seen. Vessels waiting for a berth at port are being staged (at anchor) outside the port in record numbers. One key distinction compared to other congestion years is the larger size of vessels deployed now. The average size of vessels at anchor in February were ships that could hold 14-15,000 TEU (Twenty Foot Equivalent) containers. In 2015, the last major congestion, the largest vessels sailing was 10,000 TEU. The challenges we are facing are amplified by the larger vessels in the trade today.

The takeaway from this situation is loaded containers will be delayed coming into the US, but the larger challenge is vessels will quickly get out of rotation in their regular schedules, thus creating missed sailing opportunities back in Asia.

The long-term forecast for 2021, is that until demand for imports slows substantially, not much is going to change in ocean trade. Capacity will remain extremely tight into Q4 of 2021 and equipment imbalances could also add to that scenario. Contract ocean import rates for 2021 (established on May 1st) could be as much as 60-100% higher compared to 2020 rate levels. In conclusion, for much of 2021, most import customers are going to struggle to find capacity and they will be paying significantly higher rates compared previous years.

ABOUT SUNTECKtts

With over 200 offices throughout North America, we solve a vast array of domestic, international, air, and ocean transportation challenges. Our shipping expertise encompasses small parcels, LTL, truckload, intermodal, air, ocean, and supply chain solutions to ensure every need is met.